By Michael Sauer from Endorphin Wealth

In my first article, I explained the five most effective steps for getting first home buyers into the housing market. Here, I have compiled my ‘best of the rest’ guide to ensuring you are financially well-organised.

- Only pay the minimum off your HECS/HELP

Once you earn over $51,957 pa, you will be required to pay a scaling percentage of your income towards your HECS debt. Ensure you do not make additional voluntary repayments. The reason? At the risk of sounding like treasurer Scott Morrison, HECS debt is the ‘best’ debt you can have because it is only indexed by inflation each year. This indexation rate has only averaged 1.63% pa over the past three years.

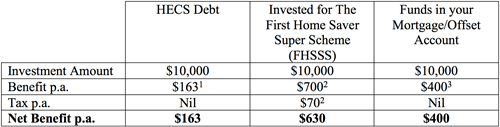

The following table compares the potential benefits of paying off $10,000 of HECS debt versus two alternative approaches:

1 Indexation rate at 3-year average of 1.63% p.a.

2 Superannuation generating 7% p.a. Assuming 2/3 income yield taxed at 15% & 1/3 capital gain.

3 Mortgage interest rate, at 4% p.a.

As the table above illustrates, it’s more effective to utilise the FHSSS if you don’t have a home loan (and want a house in the future). If you do have a home loan, your best bet is to put the funds directly into your mortgage or offset account rather than paying down your HECS.

- Life insurance – you can’t live without it

No one wants to think about death, injury or illness, but it’s essential that you get your insurances organised – the earlier, the better. Australia has a massive underinsurance problem with 38% of families having no life insurance (SMH, 2017). Most people will have default insurance within their superannuation, but it is very rarely enough to cover them or their family’s basic needs if an injury, illness or death was to occur. Life Insurance is a complex and extensive area (including Total & Permanent Disability, Income Protection (IP) & Critical Illness insurance) which is best navigated with the use of a trusted Financial Adviser who can help you with:

- Calculating the amounts of each cover you require

- Determining which insurance features suit you

- Choosing the insurer that will best suit you based on:

- Their tolerance to any existing conditions you may have

- Your occupation

- Price

- Product quality

Taking out cover in your earlier years is extremely affordable and can be paid for with your super funds leaving more money for smashed avo savings.

- Consolidate your super accounts

If you’ve opened a super account at every new job and haven’t consolidated them into one super fund, you could be wasting hundreds if not thousands of dollars per year. The two main issues are:

- Duplicate administration fees

Most super accounts have a minimum flat fee which across multiple accounts can become costly. Not only do these fees reduce your balance, you also lose out on the compounding returns you would have received on these fees which over your working life could cost you thousands more.

- Duplicate insurance policies

If each of your super accounts has insurance, you could be over-insured. This is specifically problematic for income protection insurance as you cannot claim more than 75% of your current salary as an insurance benefit even if you have multiple policies which total for more than 75% of your salary.

If you’re a DIYer, you can consolidate your accounts on MyGov or, if you would prefer an expert handle the consolidation and recommendation of your new super account, a trusted Financial Adviser can assist.

A word of warning: If you decide to consolidate into one super account but need more insurance than the default amount available, you will need to answer medical questions. At this point, you could be declined for the additional cover you need if you have existing health issues.

- Cut up your credit card

If HECS is ‘good debt’, then credit card debt is definitely ‘bad debt’. Whereas HECS debt incurs around a 1.63% p.a. cost, credit cards are generally between 10-20% p.a. If you have a credit card and can pay it off with cashflow in the next three months, do so and then cut the card up and throw it in the bin.

If you can’t pay your card off in the next three months with cashflow, you should investigate a balance transfer and begin reducing your living expenses (refer to my previous article for some quick tips on how to do this). A Canstar comparison can assist in finding the right balance transfer option for you. Once you have completed the balance transfer, cut up the new credit card that comes with it. It’s important to realise that a balance transfer is a band-aid solution and the amount of times you can do it is limited – the real problem is your cashflow spending.

If you think you’re a savvy saver and have a credit card for ‘bonus points’, take some time to determine whether you’re currently saving 20% of your after-tax income after you have cleared the credit card each month. If you are and have savings to prove this, you probably have a pretty good handle on controlling your living expenses and therefore a credit card strategy might be viable. However, from my experience, most people are failing to hit a 20% savings benchmark and are overspending rather than “flying for free” on bonus points as they tell their friends.

- Super is your friend

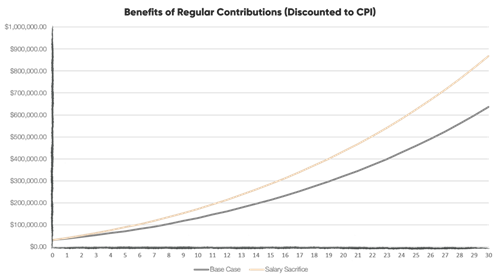

Many people pay little attention to their superannuation. In fact, 40% of Aussies don’t even know how much they have in super (MLC, 2016). This is an unfortunate missed opportunity as super is the best vehicle for long term savings given its various tax advantages. Let’s say you’re an average income earner ($75,000 p.a.), contributing 5% of your salary (above what your employer puts in) throughout your life. At retirement, you will have an extra $232,859 (in today’s dollars) by regularly contributing.

Additionally, you would also benefit from a reduction in taxes of over $65,000. Another compelling way to look at it is this: throughout your life, you would make additional contributions of $265,353 but end up with an extra $565,209 in your super at retirement (in future dollars).

Having followed the tips in these two articles, you should be well on your way to seeing the positive impact that sorting out your finances can have on your life.

Michael Sauer is an Adviser from Endorphin Wealth, where he creates tailored financial roadmaps to help his clients reach financial wellbeing.

Article by:

Comments1

"Thanks Micheal! - Wouldn't have though that about HECS - always think it's best to wipe all debt asap!!"

Aimee 14:40 on 10 Aug 18