Remember the first time you received interest from your savings account? Whether it’s $100 or just 10 cents, it’s a magical feeling seeing “free” money appear in your account. But feelings can be deceptive, and if you think you’re earning significant money from a high interest savings account, you should look closer.

Savings accounts: what are they good for?

Savings accounts are a good solution for those with shorter-term financial goals where you can’t take any risks with your money. After all, you never see your savings account going down, like you might with an investment.

But if you’re trying to grow your money, a savings account is not the best place to keep it. As Warren Buffet said:

“Today people who hold cash equivalents feel comfortable. They shouldn’t. They have opted for a terrible long-term asset, one that pays virtually nothing and is certain to depreciate in value.”

Current interest rates

Let’s get technical for a moment. The interest rates from a high interest savings account reflect the official cash rate set by the Reserve Bank of Australia, which is currently a modest 1.50% p.a.. Currently, most high interest savings accounts shows standard variable rates ranging from 1.20% to 1.75% p.a., and bonus interest rates are in the 2.95% to 3.15% p.a. range.

The bonus rates do come with strings attached. Often the higher bonus rate applies only for a limited honeymoon period on balances up to a certain amount. Sometimes you have to add minimum monthly additional contributions to get the bonus rates. Whatever it is, to access the bonus there are usually some conditions.

As with most financial products, the devil is in the details, read the terms and conditions of any bonus rate carefully.

What you see isn’t what you keep

At first glance, it might appear that high interest savings accounts are an easy way to make “free” money. But is this really true? When you account for inflation and tax, you’ll see that the rate of return is much smaller than you’d think.

In investing it’s not what you earn but what you keep that matters. And to calculate that, you need to subtract the costs, taxes and inflation. At Clover we call this the “hip pocket return”, and it’s the only return that matters to savvy investors.

Putting your money to work

What if you put $10,000 into a high interest savings account five years ago? What would it be worth today?

To look at the real worth of our savings account, we need to adjust the account balance as we see it in our account for two key items — inflation and taxes. Inflation erodes the purchasing power of money — basically, a dollar today is not the same as a dollar two years ago in terms of its real worth. The purchasing power of a dollar today is lower than what it was two years ago due to a general increase in prices of most goods and services ranging from a loaf of bread to a haircut.

Any interest we earn on our savings account is treated as income and is taxable in the year it was paid. So without adjusting our savings account balance for inflation and the tax on interest earned, we don’t know the real worth of our account.

In order to estimate the real worth of $10,000 invested in a high interest savings account five years ago, we can use the historical interest rates on retail savings accounts/bonus accounts and adjust the data for inflation and tax impacts.

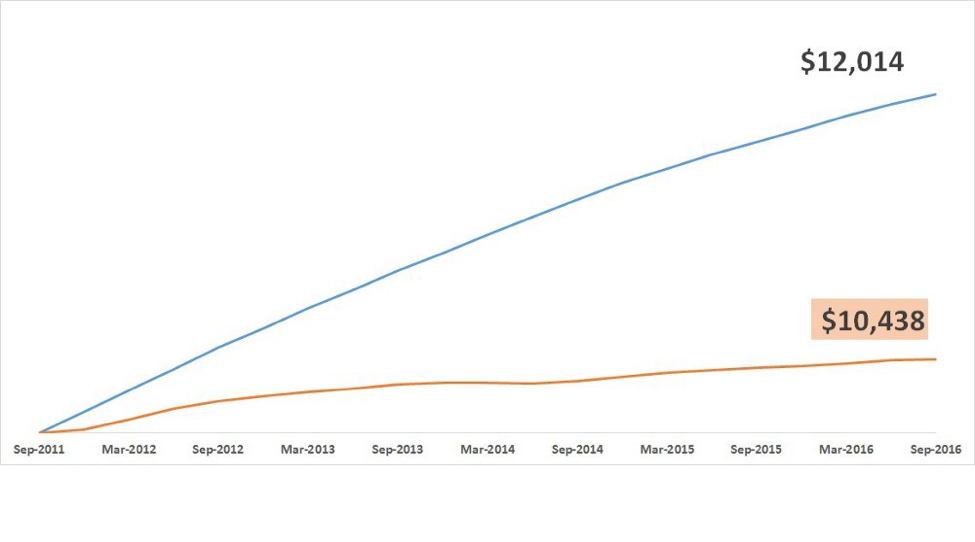

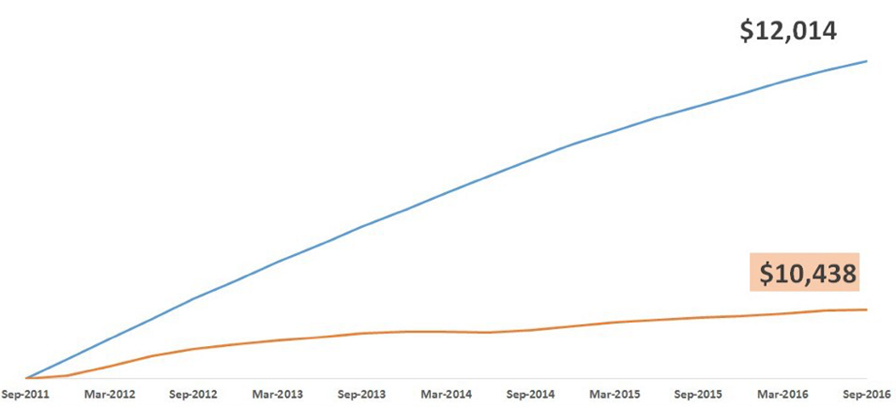

As the chart below shows, $10,000 invested during 2011 in a high interest savings account would have grown to $12,014 over the five year period. after adjusting for the effects of inflation and tax however, the $12,014 is only worth $10,438, a return of 0.86% p.a. over the five year period.

What? Save $10,000 for five years and get a miserable $438 increase in the purchasing power of your money?

Unfortunately, yes.

Rock bottom savings account returns isn’t a recent phenomenon. Data going back to 1900 suggests that savings accounts have a real rate of return of 0.7% p. a. over the 116 year period. This real rate of return is only adjusted for inflation and doesn’t even take into account any tax impacts.

This is especially relevant if you’re savings for a deposit on a home. Avocado toast aside, property prices in Australia have risen significantly faster than general inflation and you could end up further behind each year if your savings aren’t keeping up.

No risk, no reward

The results of our study into savings accounts confirms one of the foundations of investing: that risk and return are intimately entwined, and that you cannot expect to be rewarded without taking some measure of risk.

If you want your money to work for you over the longer term, investing in assets such as shares and bonds is key.

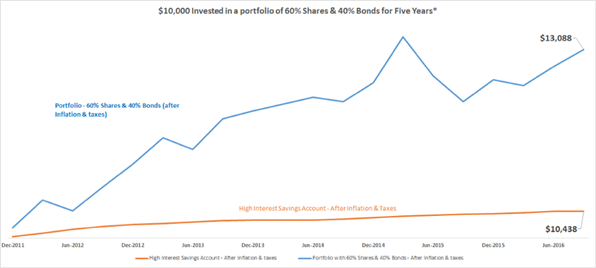

For example, below we compare how a portfolio invested in 60% shares and 40% bonds would have performed over the same five year period, adjusted for inflation and tax impacts.

High Interest savings account after inflation and taxes = $10,438; Portfolio with 60% Shares and 40% Bonds after inflation and taxes = $13,088

As expected, investing in higher risk/return asset classes such as shares and bonds does produce significantly greater returns than a high interest savings account. The flip side is that higher risk asset classes are also more volatile, with their value going up and down a lot more.

Different asset classes have different rates of return, and these rates vary greatly between the different asset classes — the table below is only a selection of options. Even though a “low risk” high interest savings accounts can earn you 2.5% p.a., you risk not achieving your goals altogether because of the lower returns.

The verdict

High interest savings accounts are “safe” — you won’t see your money decrease. But they present a different kind of risk — the risk of not taking advantage of excellent, historically-proven ways to grow your money, and the risk of not meeting your financial goals effectively.

If you’re planning to hold money in a savings account for an extended period of time, you may want to consider investing in a diversified portfolio which carefully considers not just your return objectives but also your risk tolerance. If you have a lower risk tolerance, a conservative portfolio holding with a higher percentage of bonds is one way to invest with less risk.

Making the jump from a high interest savings account to a diversified portfolio can be scary — but learning about how financial risk works can help you understand how different approaches can work better for you. And with the internet at your fingertips, there’s no reason not to start learning today.

This article was first published on Clover.com.au where notes and sources are attributed.

Article by:

Comments1

"Wow. Less than 1% return over 5 years? That's criminal!"

Shocked 15:07 on 14 Sep 18