What is in the water cooler at ASIC? Or is there something strange in the air conditioning units of the shared offices frequented by our newest licensee entrepreneurs? Why has a two-year trend to fewer and larger licensees suddenly reversed? Are we returning to the heady days of post-FOFA 2014 when we saw an explosion of new licences formed?

This all comes at a time when the proposed compensation scheme of last resort (CSLR) is up for consideration in Parliament and inclusion in the May Federal budget. Unsurprisingly, formal submissions and other commentary is now surfacing as key stakeholders make their case for this important consumer protection initiative.

Countplus CEO Matthew Rowe made some strong statements this week about the financial viability of Australia’s Top 50 licensees, suggesting that not one of them is achieving an adequate risk-weighted return on capital. His analysis is a backward looking one based on analysis of published financial statements, so the situation is likely to get more dire initially with the December 2020 removal of investment commissions and rebates that have supported many of these businesses over the years.

Our own survey of the Top 300 licensees late last year painted a very different picture, with more than 70% of respondents generally happy with their profitability, were anticipating growth in adviser numbers, reported very low debt levels, and every single one of them was satisfied with their capital adequacy to meet regulatory obligations. Interestingly almost 60% of respondents had less than $5m in revenue.

It’s a strikingly different perspective to Matthew’s observations, but are we comparing the same things? Capital adequacy to meet regulatory obligations is arguably a much lower hurdle than having the financial capacity to accommodate, in relative terms, the kind of remediation costs that the aligned licensees have had to deal with following the Royal Commission. For many smaller licensees, these liabilities are probably still unknown / undiscovered and very likely not adequately provisioned for on their balance sheets. Let alone the other investments these businesses may have to make in positioning their businesses for an advice 2.0 world.

The financial hurdles for licensees under RG166 simply require them to “remain solvent” and meet a “cash needs requirement”. ASIC acknowledges that it is not a prudential regulator and therefore does not impose capital adequacy obligations beyond these basic provisions.

This is part of the narrative emerging around the CSLR. Should ASIC have tougher capital adequacy requirements for new licence applications, and existing ones? And could the licensee population fund such an impost, no matter how gently it was introduced, and notwithstanding our own licensee survey that suggests the majority of survey respondents are in the pink financially?

It’s possible these considerations are front and centre for FPA, whose submission this week pointedly called for the CSLR to be a “broad-based model drawing from all sections of the financial services industry”, no doubt a reference to product manufacturers pulling their weight more substantially and softening the blow for advisers. Something that seems quite likely, particularly with the Design & Distribution Obligations legislation implementation, coming in October, already holding manufacturers financially responsible for product failures.

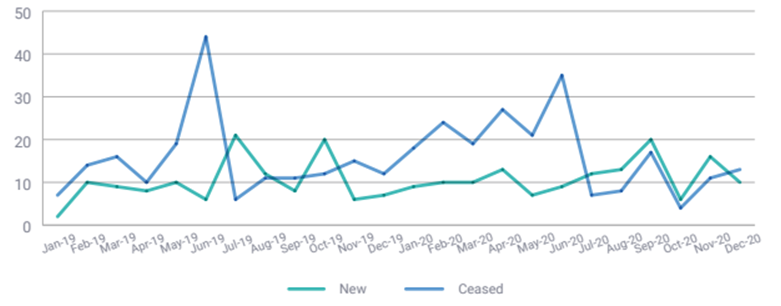

Meanwhile, as discussed in our latest Q4 2020 Musical Chairs report, the licensee registration train rattles along with seemingly little concern for all this capital adequacy hoopla. From Figure 1, the volume of new approved advice licensees has reversed a two-year trend for the second quarter running. Once again, more licensees are being established than are being discontinued, with the lion share being small self-licensed boutiques staffed in many cases by advice teams emerging from the aligned groups like AMP, IOOF, MLC, and ANZ.

Figure 1 – Newly Registered Licensees vs Discontinued Licensees 2019-2020

Source: Musical Chairs report Q4 2020

Interestingly, 65% of firms that had their licence cancelled or suspended by ASIC in the last 12 months was due to financial governance or sustainability issues. But that amounted to nine firms which represents 0.4% of all licensees. If things are so rosy, why do we need a CSLR? Or is this picture of financial rude health really fiction, and further evidence of the limited surveillance resources of ASIC?

I am reminded of some global research that said only 4% of businesses from all industries reach more than $1m in revenue and only 0.4% ever make it to $10m. Sub-$10m would cover roughly 95% of the licensee market. Something doesn't add up, you do the maths.

Article by:

Comments1

"In relation to the last paragraph, where a licensee of 20 planners are all generating $500k each, the licensee is probably reporting revenue of $10m. If we assumed 90% of that revenue simply passes through the licensee to the planner, then how much revenue does the licensee generate? $10m or $1m? It's my understanding that by accounting methodologies and ASIC requirements they're right to report the $10m - but that's really only a result of the regulatory requirement that a planner be paid via a licensee. If the licensee was measured against other industry norms (as per the global research) and they're recordable revenue was the fee they charged for the service they provide (and not the fee they pass through) then I'm sure it would paint a very different picture. How many licensees do you expect would declare they can't meet their licensing requirements? I think your survey proves that answer - none. "

Ryan.G 11:37 on 12 Feb 21