This is the second instalment from Mark Pesce, following his overview of the cryptocurrency market. We take a look at the development that has made cryptocurrencies stand out - Blockchain Technology. If you’re unsure what the blockchain is, renowned technologist and futurist, Mark Pesce reveals with this simple explainer, that it’s not that hard to understand.

BLOCKCHAIN BASICS

Money must have two essential features: it can be counted, and it can’t be counterfeited. As a result, it’s possible to know how much money someone has, and after counting, it can be verified as authentic. Neither of these work perfectly: crooks cook the books to make themselves look richer than they appear, and even the most sophisticated banknotes can be copied.

Like money, cryptocurrency ownership can be verified, and cryptocurrencies are almost impossibly hard to counterfeit. These qualities come from the basic technology enabling the cryptocurrency revolution, something known as the ‘blockchain’. That word gets thrown around a lot without any explanation - as if it were too complicated for any but boffins to understand. Yet there’s nothing hard to understand in the operation of a blockchain, as you’ll see in this example.

For someone who travels a lot on business (as I do), travel reimbursements are a necessary evil. There’s a real need for transparency in the reimbursement process, to keep all parties comfortable that they’re being dealt with fairly. So after a trip to Adelaide, I take photographs all of my receipts - taxi, flights, accommodation - gathering these photographs together into a single package. Lastly, I’ll create a ‘signature’ (technically known as a ‘hash’) that uniquely reflects these receipts. Why do I need this signature? It’s a form of guarantee: should anyone change so much as a single pixel on any of these receipts, the signature changes completely.

I gather up the photos of my receipts and the signature and put them into a ‘block’. It might look something like this:

Fig. 1 - Block 1

Fig. 1 - Block 1

A few weeks later I make a trip to Melbourne, and following the trip, I again take photographs of all my receipts, gathering them together into a single package. Just before I add a ‘signature’ to these receipts I do one very important thing: I add in the ‘signature’ created from my Adelaide receipts. Why am I doing this? Let’s say someone wanted to tamper with my Adelaide receipts: They could alter a receipt, then generate a new signature to match the newly altered receipt. There’d be no way to catch that, because everything would look like it was in agreement. But as soon as you put the signature from the Adelaide trip into the collection of Melbourne receipts it becomes much more difficult to change the Adelaide receipts, because you have a copy of the Adelaide signature to compare it against inside the Melbourne receipts.

After the signature from Adelaide has been added, a signature is created for the Melbourne receipts. That new ‘block’ might look like this:

Fig. 2 - Block 2

Fig. 2 - Block 2

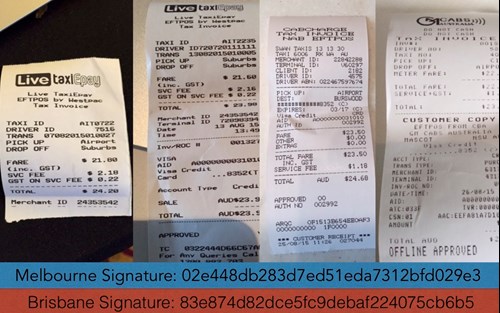

Finally, I make a trip to Brisbane, and, once again I photograph all of those receipts, gathering them together. This time I take the signature from my Melbourne receipts and put that signature into this block before I generate its signature. Now no one can tamper with the Melbourne receipts, because that will change the signature of that block, which means no one can tamper with the Adelaide receipts, because that signature is recorded in the Melbourne block.

Fig. 3 - Block 3

Fig. 3 - Block 3

These signatures ‘chain’ the blocks together. As the chain grows, earlier links in the chain become progressively more difficult to tamper with. Any block that’s more than few links deep in the chain is effectively set in stone, preserved forever. My travel receipts can no longer be forged, but they can always be verified - by anyone who wants to inspect them. Both I and my clients can agree on how much they need to reimburse me, and we can both rest assured that neither of us have tampered with the receipts.

Fig. 4 - "Blockchain"

Fig. 4 - "Blockchain"

This chain of blocks - or blockchain - creates a ledger that is open, inspectable and verifiable. Exactly the kind of thing you’d need to move money from one account to another. Cryptocurrencies like Bitcoin are simply much larger versions of these ledgers. Every transfer from one account holder to another is visible, verifiable, and can’t be forged - because it’s on a blockchain. That’s how you and everyone else can verify that your Bitcoins really are yours.

And now you know how a blockchain works - that wasn’t so hard, was it?

Mark Pesce is a futurist, inventor, writer, entrepreneur, educator and broadcaster with 35 years experience working in technology, He holds honorary appointments at the University of Sydney and UTS.

Article by:

Comments8

"This is a great articles. Thank you for posting."

Alison Haynes 15:57 on 15 Jan 18

"Thank you Mark, great explanation and the first time I've seen any such explanation. Now I can hopefully progress with further understanding of how it all comes together. One question that's been burning in my brain lately is: How come (est) $20 mio of BTC went missing a few weeks ago (evidently)? Knowing how / why that happened would go a lot further in helping my overall understanding in this area. Thanks and regards, Richard"

Richard 16:54 on 12 Jan 18

"Fair enough Geoff - it's a bit beyond me. But if BCKing is right and it threaten banks I still think it will have a hard time going anywhere."

No Trust 15:53 on 12 Jan 18

"I actually spoke with my adviser (not naming names) over the Christmas break and was astounded how little he knew about the technology. I told him quick smart he needed to get on top of this - it wasn't fair I'm an IT Director, but advisers need to be on top of this. It will change most businesses and people's investments like the internet has done."

David Green 15:36 on 12 Jan 18

"Hi No Trust - it’s more secure than the centralised banking system. The decentralised nature of blockchain makes it secure. It also means there can be multiple backups of the blockchain globally that’s not connected to anything. I think you’ve missed the entire point. Banks are more vulnerable to “someone pulling the plug” as you call it."

Geoff 15:01 on 12 Jan 18

"I just don't trust this type of electronic tech. Surley sooner or later some computer whiz will work out ways to infiltrate/crack/corrupt this. If the only record is digital what happens when someone pulls the plug? An EMP blast could fry electrics and there would be no way to check records? It might have use but it won't replace money."

No Trust 14:39 on 12 Jan 18

"This seems like a really simple explaination. I had no idea how the blockchain worked. Is it really as simple as this? "

Andrew Greene 14:30 on 12 Jan 18

"Blockchain will ultimately prove the downfall of banking - banks act as intermediaries with appropriate systems, both human and technology that act as the ledger between buyers / sellers & depositers / lenders. Blockchain will replace all this. In addition, one of the core assets of a bank is the data they currently hold on their customer base - with the government's open data banking policy, we will suddenly see a swathe of competitors who are not beholden to shareholders chasing a particular ROE or having to look at their CAGRs. Roll out the bell - the fat lady will soon be singing!"

BCKing 13:59 on 12 Jan 18