"If I have greater than$1.6m in Super but my spouse has very little Super, can I utilise the bring forward rule to transfer up to $300,000 from my Super to my spouses super? Alternatively if I have up to $300,000 in a separate bank account outside of Super, can I contribute those funds into my spouses super?"

Rikki from Adelaide

Top answer provided by:

Anabel Reign

Dear Rikki,

Thank you for your enquiry and for such an excellent question.

The Transfer Balance Cap (TBC) needs to be addressed first in order answer your question completely.

The government’s intention in 2017 was to create a Superannuation Reform which would improve the retirement economy for our aging population. To do so, they introduced this TBC to even out the tax advantages being utilised by high net worth funds and to instead direct these strategy options to increase funds with lower balances.

This strategy is quite complex and, in your case, could impact your hard-working retirement savings; So, you are doing the right thing by sourcing a way to make superannuation strategies work for you.

To know which strategies are now available, let’s first consider this legislation.

The relatively new Superannuation Transfer Balance Cap (TBC) is a $1.6m maximum can be treated as tax-free once in pension phase.

Within this cap, each person has a Transfer Balance Account (TBA) that broadly operates on a system of credits and debits, like a bank account. The purpose of the TBA is to track the net amounts transferred to (and from) pension phase. This TBA is what determines whether you have exceeded your transfer balance cap on any given day.

An individual in accumulation phase that has excess of $1.6m is still able to leave this in superannuation, however, an Excess Transfer Balance Tax (ETBT) would be payable on the accrued amount of earnings above that $1.6m.

The first ETBT is 15% yet it jumps to 30% tax on earnings for subsequent breaches. So, it is wise to avoid exceeding your $1.6m balance where possible.

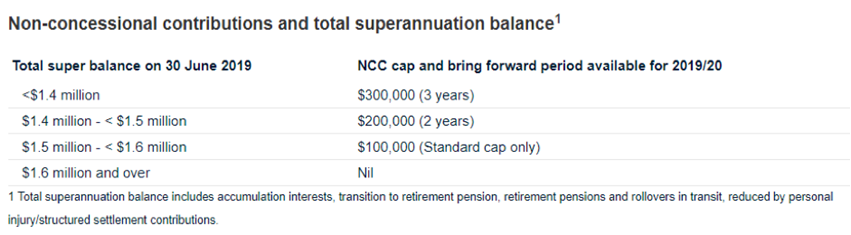

Your consideration to use the Bring Forward Rule of $300,000 would normally be ideal as Non-Concessional Contributions (NCCs) are not taxed by the receiving fund. As you’re aware, there is a limit to the amount of NCCs that can be made without incurring a penalty.

Normally a person could contribute up to $100,000 per year without paying tax on the contribution. If a person has a lump sum or is approaching retirement they could ‘Bring Forward’ three years and instead make a $300,000 contribution tax free.

Effectively the TBC restricts the amount of contributions that you are now able to make tax-free. This does not however restrict you from contributing to your spouse’s super. Though this does depend on personal considerations such as marital, taxation and estate planning circumstances.

Assuming you are preferably over 60 or eligible to withdraw super; and your spouse is still eligible to contribute to super and hasn’t utilised their NCC limit in the past three consecutive years, there may be the following options:

Option A

As questioned, you could utilise bank account monies to make an NCC of $300,000 directly to your spouse’s super. This would reduce the amount of tax you pay on those personal funds from your marginal tax rate to 15%.

Option B

As you are close to accruing ETBT, consideration could be made to instead withdraw $300,000 from your super and contribute this as an NCC to your spouse’s super.

Option A + B

To utilise the above options together, a smaller portion (e.g. $150,000) of your super could be withdrawn to reduce the risk of ETBT, and the (e.g. remaining $150,000) could be contributed from your personal funds to make the total NCC $300,000.

As noted, it is crucial to consider what income you have for retirement well in advance as leaving superannuation to ‘run its course’ can have many implications regardless of your balance.

Understanding what these strategies mean for you and receiving appropriate advice is critical when considering tax effective retirement planning.

I hope this is of help.

Warm Regards,

Noni

While the Adviser Ratings Website facilitates the question and answer functionality, all such communications are between users and authorised financial advisers, of which Adviser Ratings has no affiliation. Adviser Ratings is not the advice provider and does not provide financial product advice and only provides information that is general in nature.

Article by:

Comments1

"Also, Option C by utilising the bring forward rule, why not consider $400,000 NCC contributions between now and say July, ie next financial year. How you do this, is let's say you decided to withdraw $100,000 this year to contribute to your wife's Super as NCC. Then in July, provided you are able to contribute, and can utilise the bring-forward rule, utilise the $300,000 you hold outside of Super to again make a NCC contribution, this time of the maximum $300,000 amount. You have therefore gotten an additional 33% again into a concessionally taxed environment. "

James Penner 11:43 on 15 May 20