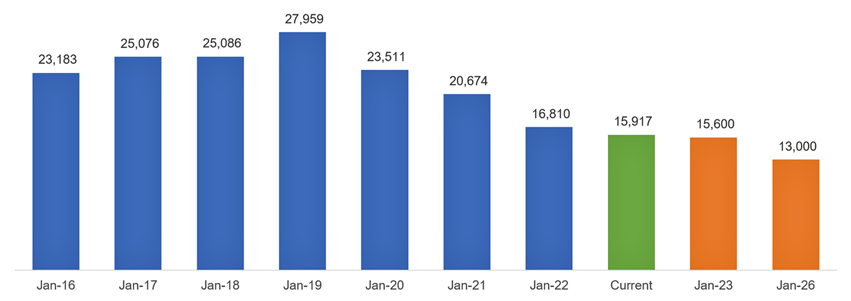

We’re only halfway through October, but it’s already been a grim month for adviser numbers, with the figure dipping below the 16,000 mark for the first time.

In the year to date, more than 1000 advisers have exited, with more expected in the coming quarter. Given September was the final chance for advisers who had twice failed to pass the exam, we anticipate further departures related to that, albeit with some time lag as information is entered into the Financial Advisers Register.

Having said that, the infamous ‘October cliff’ – a drop off in numbers as Financial Adviser Standards and Ethics Authority qualifications are updated in the register – has certainly materialised. At the start of the month, the profession said goodbye to almost 2 per cent of its remaining advisers, while just eight new advisers joined. In other words, the profession lost almost 30 advisers for every new recruit.

Adviser Ratings has long said more needs to be done to foster a pipeline of new talent, especially given the monthly new adviser figures still sit in single digits. Since 2018, the number of departing advisers has consistently dwarfed the number incoming, which has had implications for the availability of advice, adviser workloads and client fees.

Figure 1: Adviser number predictions

Source: Adviser Ratings

Loss of experience

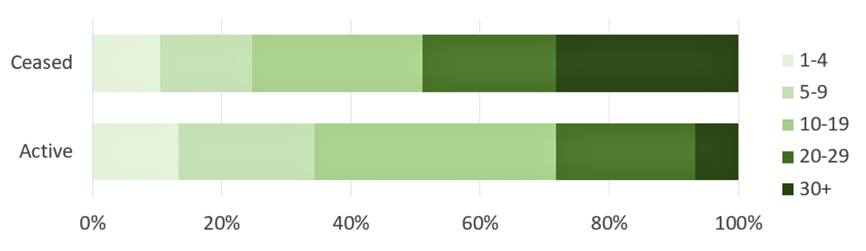

As new advisers trickle into the industry, our analysis from early October shows a high volume of advisers who departed had decades of experience. In fact, 50 per cent had been in the industry for more than 20 years and 30 per cent had been practising for upwards of 30 years. We anticipate many of these advisers won’t return to the profession unless regulatory changes are introduced following the Quality of Advice Review and the promised experience pathway.

Figure 2: Advisers years of experience

Source: Adviser Ratings

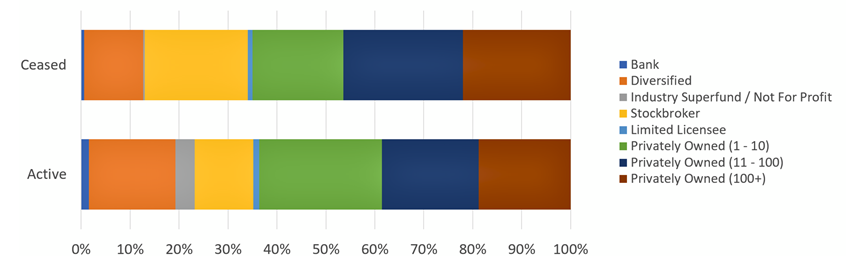

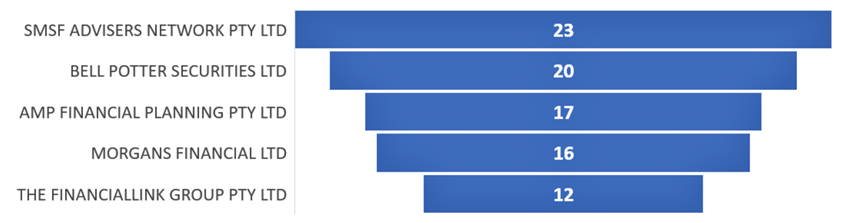

Once again, a number of licensees representing the SMSF/accountants, diversified and stockbroker spaces suffered heavy adviser losses. It has been a recurring theme for the former, as accountants have moved out of the limited licensee market. For example, the SMSF Advisers Network lost 22 advisers in the first week of the month, which lowers its total to 243 – a drop of 78 per cent since 2018.

Figure 3: Adviser Type Spread

Source: Adviser Ratings

Bell Potter, Morgans, AMP and Charter Financial Planning also lost more than a dozen advisers at the start of the month, with AMP’s adviser footprint now down 62 per cent since 2018.

Figure 4: Top 5 ceased by licensee

Source: Adviser Ratings

More than three-fifths of advisers are now operating under privately-owned licensees, with private boutiques now occupying about a quarter of the licensee market. Meanwhile, less than 2 per cent of advisers are operating under bank-owned licensees, as the Big Four continue to wrap up their wealth presence.

We will have a full wrap up of the quarter’s adviser movements in our upcoming Musical Chairs feature.

Article by:

Comments9

"It's never been a better time to be an Adviser and focus our attention on great client relationships, ignore the "white-noise" and simplify your offer."

Dave Dyson 18:14 on 19 Oct 22

"Josh Frydenberg and Jane Hume have virtually destroyed the industry. Expect far more exits when ridiculous compensation scheme is charged to advisers instead of product manufacturers and the ASIC tax is fully charged. A Liberal government is not meant to be so anti small business - their new taxes and red-tape has no benefit to consumers whatsoever."

ex-liberal 15:59 on 19 Oct 22

"This happened in the UK just after I migrated in 2006. The advisers who worked through a lot more regulation are now doing really well. I left school at 16 with no qualifications and am now almost 58. I have not found the Australian regulation troublesome, and completing the degree so far has not been too hard and only have one unit to go. The opportunity is huge and the few new advisers are missing the most important part of being an adviser, people and listening skills. They cannot be taught via on line courses and why would a successful adviser want to spend so much time mentoring and training a new adviser when also having to pay them. When I joined in 1988 one taught an adviser the communication skills and benefited from their success, although in those days there were no salaries to pay. Those who bite the education bullet will not regret it."

D Widlake 15:48 on 19 Oct 22

"Government, the Public Service sector and big Business are so entrenched in "PROCESSES," that they are incapable of making necessary changes in a timely manner. Every man, woman and dog, knows the problem and the solution has been yelled from the rooftops, though the merry go round of meetings, investigations, analysis from everyone, including from the vast majority who have NO idea, or have vested interests to continue until they have taken every dollar they can grab and stuff everyone else, is considered by people who have NIL or LIMITED knowledge, experience and ability to know what is correct and the best course of action, from the bad or worse options presented. Stephen Jones is on the right path, with a lot more needed and as much as it hurts for the thousands of Advisers who were forced to sit more exams and have their prior qualifications and ongoing education thrown back in their faces, the facts are that the current model is failing badly and MUST be changed to make it attractive for new entrants, students in Uni, people from outside our Industry and even exited Advisers, to even want to consider making a career, or returning to the Financial services Industry in a capacity that Employers can work with them and still make a profit. While we wait, more and more and more Advisers go, while the price to attain advice gets further away for most people, let alone the fact that Life / Disability Insurance premiums have doubled due to insufficient numbers of Advisers that are left who want to, or are capable of working in the wealth protection area, write sufficient New Business and help protect what premiums are in jeopardy of going off the books."

Jeremy Wright 15:45 on 19 Oct 22

"Industry super funds are the only winners and trade unions are laughing all the way to the bank, now their mates in charge are going to get rid of best interest duties (which industry super have never and will never meet). You can feel them putting the final nails into the coffin that was the advice industry.... "

Anonymous 15:42 on 19 Oct 22

"Make way for a green advisers to take over from all the experienced advisers that have dropped off the FAR. Great work and once again the consumer will be punished. Note, there's a couple of million orphaned clients, this time next year, double that number."

C Heppingstone 15:35 on 19 Oct 22

"It will only get worse as January 2026 ticks closer. Unless there is some extreme changes come in the December report on our industry it will be a complete disaster from an under insurance position that we know will flow on through the health services and Government assistance services { Centre link Medicare etc }. and that's just the start. If Commissions are scraped you wont have to wait until 2026 the damage will start immediately. Someone needs to put their hands up and say we were wrong ! This has to change not a 'tinker" here and a" tinker" there. A full blown "overhaul". "

disappointed 15:27 on 19 Oct 22

"The idiot-politicians ignored this predictable outcome in pursuit of winning the popularity contest which included head-kicking decent advisers. Even if they reduced the regulatory burden, I will maintain my high fees (supply & demand). Easier solution would have been to impose the death-penalty (figuratively speaking) on the bad apples. Customers will continue to suffer, now."

Lucy Russo 15:21 on 19 Oct 22

"The system has become more complicated and regulated and unfortunately there hasn’t been the crossover of training up for the next generation to be prepared. The Tax & Pension System needs to be simplified to benefit the Australian population and Financial education to start earlier."

Christine Ferguson 15:16 on 19 Oct 22