Not long ago, the licensee market was a magnet for some of the biggest and most powerful players in the wealth space, as well as others who wanted to participate with more limited scope.

In the past few years, however, there has been a seismic shift, most notably with the banks all but exiting the licensee arena. The presence of banks in advice has dropped more than 80 per cent since 2017, with just a few hundred advisers now officially falling under bank licensees.

More recently, we’ve seen other big players following suit, by either leaving the licensee market completely or drastically reducing their presence.

Segments in decline

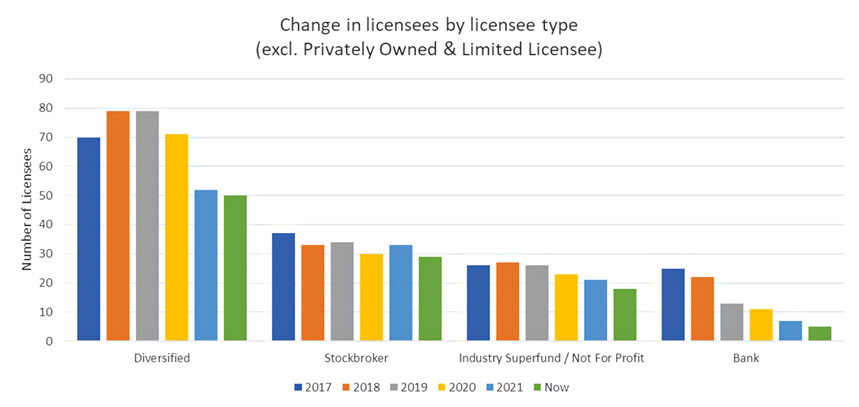

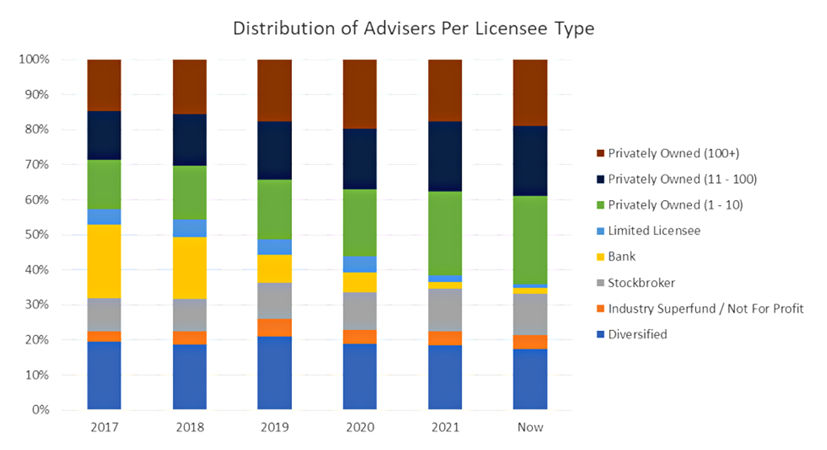

As Figure 1 shows, the bank licensee decline has been unparalleled to date, but we’ve also seen large drops in the number of diversified, industry super fund/not-for-profit and stockbroker licensees.

Since 2017, the number of industry super fund/not-for-profit licensees has fallen by almost a third. Meanwhile, diversified licensees fell 29 per cent over the same period, with the steepest drop happening in 2020.

In the stockbroker segment, we’ve seen a 22 per cent dip since 2017. In 2021, licensee numbers in this cohort rebounded slightly, but have more recently retreated again.

Figure 1 – Drop in licensee segments

Source: Adviser Ratings

Segments evaporating

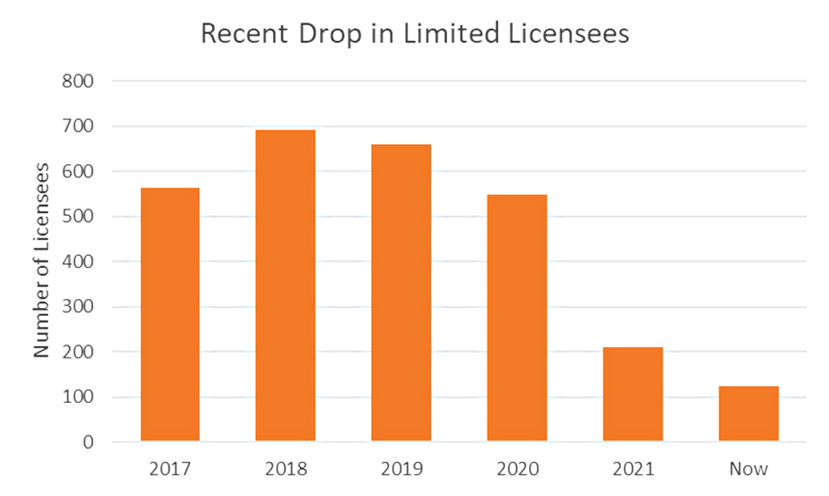

However, those declines don’t come close to what’s happened in the limited licensee market.

Just as quickly as accountants flooded into the limited licensee space to advise on self-managed super funds, we’ve now seen the market slide. Between 2020 and today, the number of limited licensees has fallen 77 per cent as accountants have wound up their licences. The SMSF Advisers Network has also experienced heavy declines.

Accountants say the limited licensee model no longer makes sense, with Chartered Accountants ANZ calling it “unworkable”.

Figure 2 – The rise and fall of licensees

Source: Adviser Ratings

Changing adviser preferences

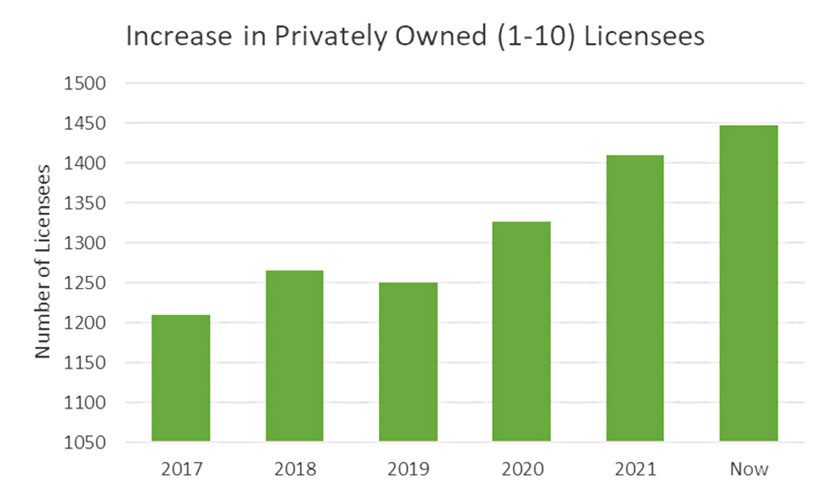

In addition to AFSLs folding, we’ve seen advisers’ appetites for big licensees wane. For hundreds of advisers, this has meant establishing or moving to boutique licensees. This trend has contributed to the privately-licensed segment taking up a much bigger share of the pie. In fact, two-in-three advisers now operate under the private model.

Figure 3 – Small licensee growth

Source: Adviser Ratings

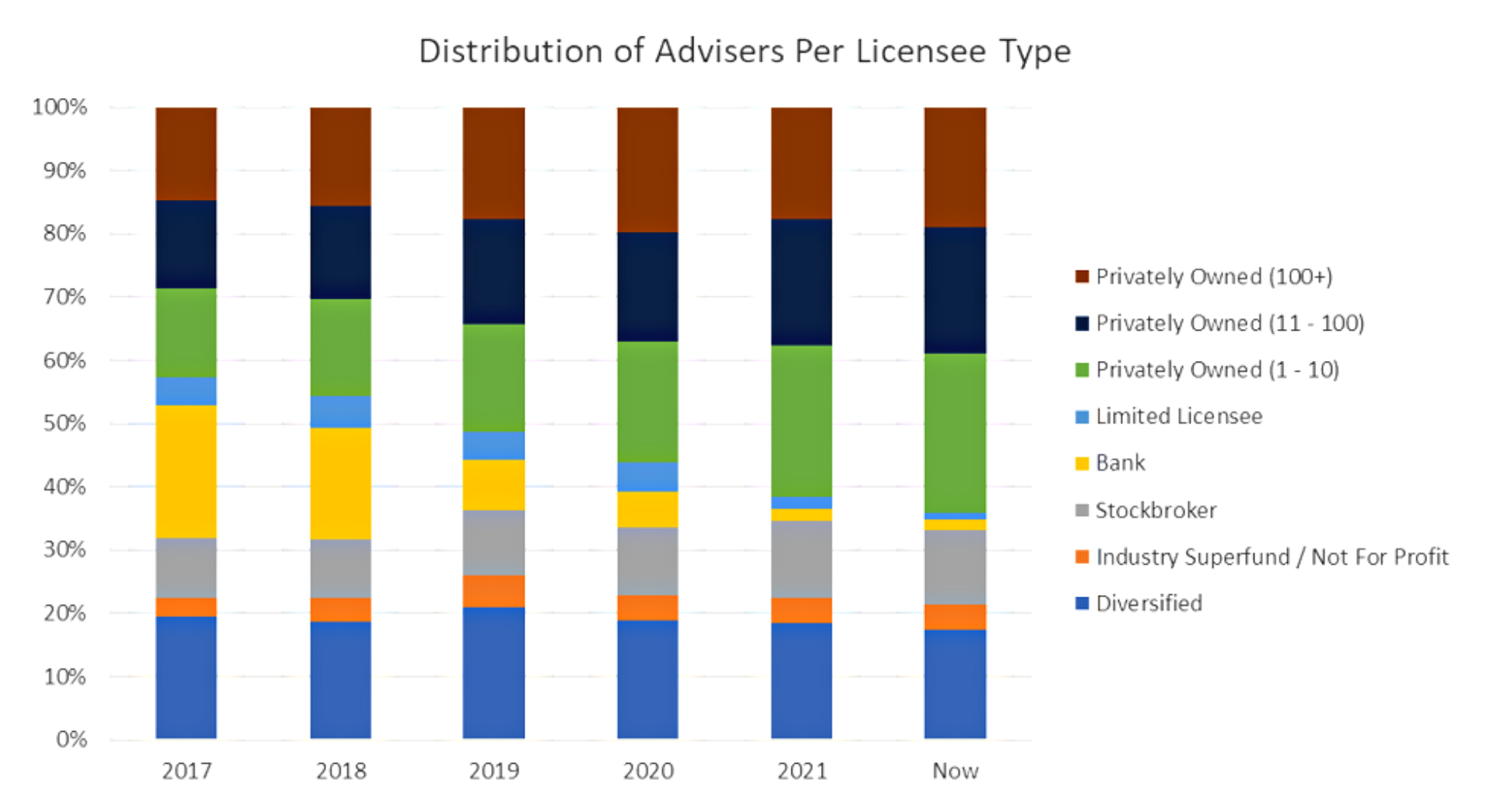

Figure 4 – A changing spread

Source: Adviser Ratings

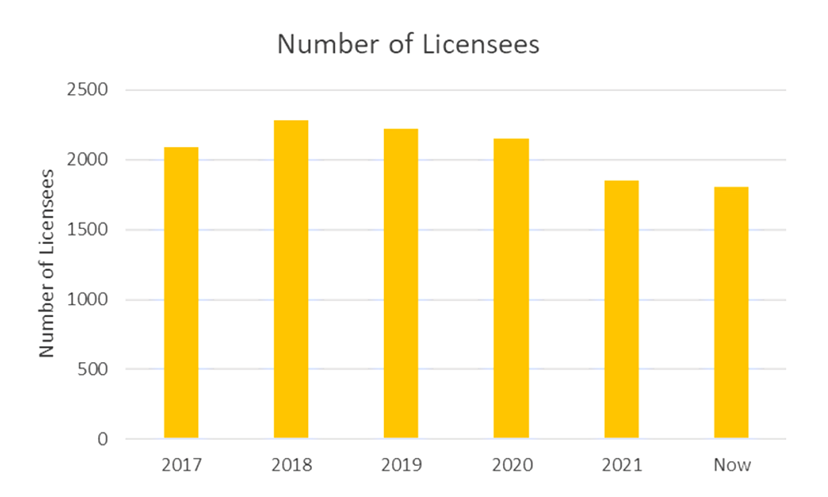

Despite the emergence of more solo and boutique licensees, however, the overall volume of AFSLs has been steadily dropping since 2017. With adviser numbers continually falling, the number of licensees dropped below 2000 for the first time last year.

Figure 4 – Falling licensee numbers

Source: Adviser Ratings

Article by:

Comments0