While advisers have been using technology to support their practices for several years, we’ve recently seen an acceleration in the availability of smart tech solutions.

Artificial intelligence applications, such as ChatGPT, are being integrated more widely into several industries and we expect advice to be no exception.

In her final report to Treasury, Quality of Advice Reviewer Michelle Levy said she believes technology and digital advice tools will increasingly be used to complement traditional advisory services.

“There is every reason to think that the technology will continue to improve such that there will be more and more cases where the advice provider will be a computer program or algorithm, while the human adviser, where they are involved at all, will be the intermediary between the program and the customer,” Levy said.

The key question: How will advisers embrace and integrate this technology?

With that in mind, we thought it would be worth taking a look at data from our last Landscape Report to see how advisers have been using solutions to date – and where they are keen to expand.

Technology and practice efficiency: the landscape and appetite

Amid fears about compliance and regulatory change, we didn’t see a huge shift in the use of new efficiency technology from advisers last year. However, data from the Netwealth AdviceTech report showed there was a strong intention from practices to further integrate tools for online fact-finding, risk-profiling, scaled advice and client feedback.

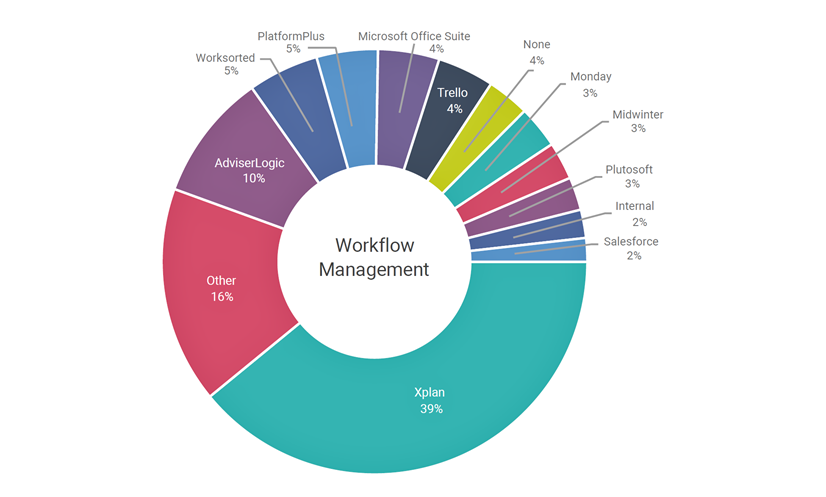

In terms of the tools used for advice production, workflow management and annual agreements, incumbents like Xplan have continued to dominate, our survey of more than 500 practices revealed.

Figure 1 – Practice uptake of workflow management tools

Source: Adviser Ratings

Post-pandemic, we’ve also seen a growing desire from advisers and clients for client portal tools where data can be exchanged easily during the advice process. Again, results from our last Landscape Report showed Xplan held more than a quarter of client portal business.

At the same time, advisers have indicated they increasingly want tools that can help their clients visualise their goals and see the impact of different scenarios. We expect this will become even more important as clients grapple with the myriad current challenges, such as rising interest rates, inflation and market volatility.

While we are still awaiting the government’s response to the Quality of Advice Review, we can’t see a scenario where technology doesn’t play a bigger role in making advice more efficient for advisers and more accessible for consumers.

Don’t forget to check out our newest data on how advisers perceive current technology providers in our soon-to-be-released 2023 Landscape Report.

Article by:

Comments0