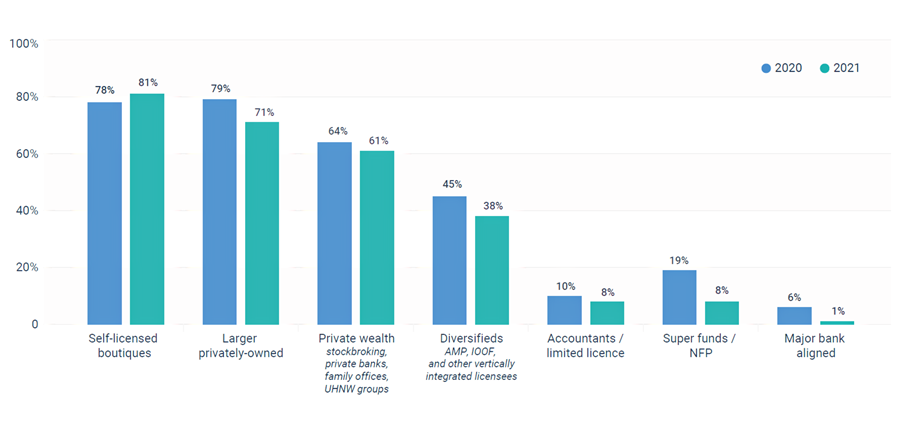

The changing make-up of the advice industry has prompted the retail sector to shift gears. We’ve seen a quick recalibration around new centres of influence – primarily the private market, with self-licensed boutiques emerging as the top target of distribution teams.

In our previous survey, distribution teams reported that they were placing slightly more attention on the larger, privately-owned licensee segment, but our most recent research shows their smaller counterparts are where distribution teams placed most of their efforts in the past year.

Figure 1 – Where distribution teams see the most opportunity

Source: Adviser Ratings' 2022 Australian Financial Advice Landscape Report

Diversified licensees – which include AMP and Insignia (formerly IOOF) have seen a year-on-year decline in distribution focus. Meanwhile, other shrinking segments – like accountants with limited Australian Financial Services Licences (AFSLs) and the big banks – are naturally receiving little attention these days from distribution heads.

To better understand retail sentiment, Adviser Ratings this year surveyed more than 70 distribution heads, including fund managers, super funds, insurers, platform providers and research and investment consultants. Our findings shed further light on where the retail sector is heading.

From banks to boutiques

It wasn’t long ago that boutiques made up a very small piece of the retail pie, while banks owned a lot of the value chain. We’ve seen that shift quite quickly. A few years later, it’s little surprise self-licensed boutiques are capturing attention. While the Approved Product List (APL) control is a major drawcard for distribution heads, they have also noted the flexibility around technology, outsourcing and culture.

However, distribution teams told us boutiques also present time challenges, given the increasing number of decision-makers to consult.

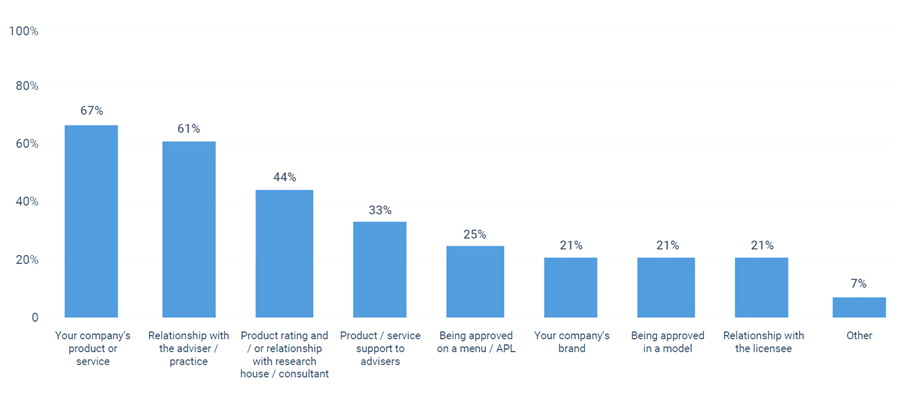

Determining distribution success

Despite that, distribution heads list the adviser relationship as the second most important factor in their success, followed by the strength and characteristics of the product itself. Consistently, distribution teams have told us being able to access the adviser or practice and convince them of a product’s merits is critical to their performance.

The relationship with the licensee is deemed less important for most distribution heads, with the exception of software providers and data companies.

While research house ratings are still considered important for success, especially for fund managers, model portfolios have been largely relegated to the past.

Figure 2 – Most important success factors: distribution heads

Source: Adviser Ratings' 2022 Australian Financial Advice Landscape Report

Understandably, the shrinking adviser workforce continues to present problems for the retail sector, particularly when combined with the increased number of decision-makers. In essence, distribution teams are struggling to cover the breadth of practices with their finite resources. Nonetheless, there’s broad recognition that there are burgeoning adviser opportunities that need to be captured, which is the primary challenge for the sector to meet.

Article by:

Comments0