New research recently published indicates that more than half of pre-retiree Australians (aged over 50) are on track to fall short of the level required to have a comfortable retirement. A lack of superannuation is the key reason behind the finding, which indicated that one third of Australians aged between 50 and 70 had less than $50,000 in super, whilst 43% had less than $100,000. The “comfortable” standard is set by the Association of Superannuation Funds of Australia (ASFA), which is the peak policy, research and advocacy body for Australia’s superannuation industry.

According to the ASFA, to have a “comfortable” retirement, single people will need $545,000 in retirement savings, and couples will need $640,000. This translates to a national average annual income of $43,695 for singles and $60,063 for couples aged around 65 years.

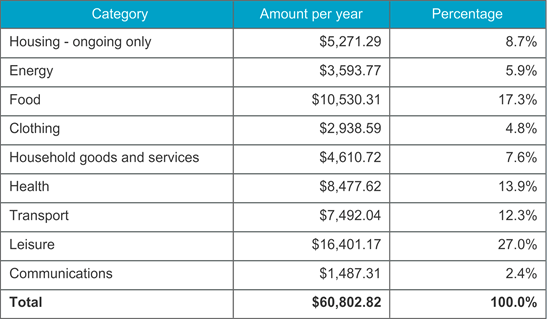

Annual Expenditure for "comfortable" Retired Couple in Victoria who own their own home.

Source: ASFA

Source: ASFA

The research published by MLC (the wealth management division of the National Australia Bank), found that almost half of Australians between the ages of 50 and 70 are at risk of falling short of the savings figures required for a comfortable retirement.

Of the 43% with a retirement saving of under $100,000, the research also revealed 42 per cent only became concerned about the balance of their retirement savings in their 50s, while over 30 per cent admitted they never checked their super balance.

The research also found that over half of those in their 50s and 60s surveyed believed their current lifestyle would be negatively impacted by retirement, leading to concerns about the standard of living they would be able to maintain once they left the workforce.

An MLC spokesperson said results were concerning, noting pre-retirees can still take meaningful action to improve their situation, including seeking out financial advice.

"We know some of the people in this age group have other assets such as property in their name beyond super, which is an important factor for them to consider when planning for retirement."

"If they don't have other assets, engaging with their super fund may prove to be a cost effective way for them to access advice in lieu of seeing a financial adviser."

As far as the definition of comfortable goes, we would encourage readers to check out the ASFA’s consumer site, which has a guide which includes the types of spending associated with “comfortable”, “modest” and “age pension only” lifestyles.

This “Standard”, is updated four times a year to take into consideration the rising price of items like food and utility bills, as well as changing lifestyle expectations and spending habits. It includes the cost of things such as health, communication, clothing, travel and household goods.

The research reinforces the importance of getting a retirement plan in place. While it is never too late to start, the earlier you can begin taking meaningful action to plan and save for retirement, chances are the better off you will be.

Article by:

Comments2

"I have believed for some years that these types of figures are inflated. The cynical amongst us may think that it is in the industry's self-interest. They totally ignore changing lifestyle as we get older and that the Age Pension still exists (though for how much longer?). It seems likely that at current interest levels many workers will not achieve these amounts of superannuation even if they work for 40 - 50 years after the introduction of universal superannuation. We do not need a research institute to tell us that older workers have much lower levels of super. The sooner people speak to a financial planner, understand the options and establish a plan the better."

Peter 17:48 on 08 Sep 17

"One can't stress enough the importance on planning for retirement. The sooner you get onto making a plan, the sooner you can let the wonders of compound interest make you better off. It should be taught in schools. I've emphasised the fact to my children and they now have substantial amounts put aside with years left to grow."

Kathy 14:37 on 08 Sep 17