“As a young person who wants to start investing, what is the safest, low-risk option that is not super?"

-Question from Belle in Dandenong, VIC

Top answer provided by:

Michael Paraskevopoulos

Hi Belle,

Fantastic question and let me start by commending you for taking an interest in investing while you're young. Time is an investor's greatest asset and starting young means more time on your side.

Every person's situation is unique and as I don't know yours, I can only offer you general advice.

Before I answer your question, I want to clarify a common misconception. Your superannuation is not an “investment”. Rather, it is a type of structure, which holds investments on your behalf.

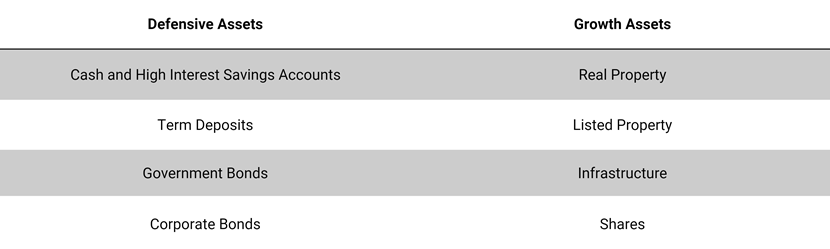

There are lots of different kinds of investments to choose from. The following table lists some traditional options but is by no means an exhaustive list. You can consider Defensive Assets as typically stable, and Growth Assets as typically volatile, but with greater earning potential.

It's important we define risk before choosing “the safest, low-risk option”. While risk can mean different things to different people, we’ll focus on the following two definitions:

- Probability of permanent loss; and

- Volatility (price fluctuations).

Based on the above, it’s tempting to stick with cash, HISA and Term Deposits, which never go ‘down’, at least not in absolute terms. Also, in Australia, the Government guarantees deposits of up to $250,000 per ADI.

But inflation erodes the purchasing power of your hard-earned dollars. If you want to truly protect the value of your money, you need a return that keeps up with inflation.

On the other hand, investing in shares or property, which are expected to do much better than inflation over the long-term, can deliver negative returns in the short-term. There’s also the risk of a single asset or class of assets doing poorly (concentration risk).

Thus, the best approach (generally speaking) is to own a diversified portfolio that holds many different investments, as it stabilizes your return while reducing concentration risk. You can achieve this through a low-cost index ETF or Managed Fund. In basic terms, rather than buying each asset individually, you can enter a Fund which holds all of the assets, of which you’re entitled to a percentage.

But diversification alone is not enough. It’s also important you achieve the right balance between ‘defensive assets’ and ‘growth assets.’

The right balance depends on your investment timeframe. If you’re going to need your money soon (let’s say less than 3 years) then you’re considered to have a short-term investment timeframe. In this instance, it makes sense to hold little-to-no growth assets and focus instead on cash, HISA, Term Deposits, and short-term bonds.

If instead you don’t need the funds for a decade or more, then you have a long-term investment timeframe and can afford to hold more in growth assets like property and shares. The right mix will depend for each person.

Belle, I can’t give you a specific recommendation as I don’t know enough about your individual circumstances, but some of the more popular managers in the diversified fund space are Vanguard and Blackrock.

If you decide to invest in a fund, you can read the accompanying Product Disclosure Statement before doing so, which outlines the minimum investment timeframe an individual should have before considering the option. It also has other information like how your money is invested and the fees in doing so.

I’ve only scratched the surface on what is a very deep, nuanced subject, so please feel free reaching out to me with any more questions that you might have. I otherwise wish you all the best in your investing journey.

While the Adviser Ratings Website facilitates the question and answer functionality, all such communications are between users and authorised financial advisers, of which Adviser Ratings has no affiliation. Adviser Ratings is not the advice provider and does not provide financial product advice and only provides information that is general in nature.

Article by:

Comments0