"I have CGT this year for my only investment property and want to prop up my super with the best tax outcome... I put $51k into super but now I think it will trigger Division 293 and think I should change it to non-concessional... I know income in Division 293 taxable contributions are the lesser of Division 293 super contributions or the amount. What is the best tax strategy?"

- Question from Pauli in Sydney, NSW

Top answer provided by:

Renee Hush

Hi Paul,

Firstly, congratulations on making such a great capital gain!

The best tax strategy is different for everyone and is based on your individual circumstances. Without assessing your individual situation in detail, it is hard to determine the best strategy, but here is some information that may help.

As tax is such a complicated area with ramifications for getting it wrong, we always recommend you seek specialist advice from a tax professional such as an accountant.

Super Contributions

Concessional contributions such as salary sacrifice, or personal deductible contributions will help reduce your taxable income and therefore, save you tax. Contributions tax of at least 15% is applied in the super fund.

Non-Concessional contributions do not reduce your taxable income and are not taxed in the super fund as you have already paid tax on these funds at your Marginal Tax Rate.

When making larger lump sum contributions I always suggest clients make Non-Concessional contributions and then claim a tax deduction at the end of the year by lodging the Notice of Intent to claim with the super fund. That way you can consult with their accountant and financial adviser to claim the appropriate amount as a deduction. This way you can make sure you do not exceed the caps or trigger Division 293 unnecessarily.

Division 293

You can find comprehensive information on Division 293 here.

In a nutshell, “Division 293 tax is an additional tax on super contributions, which reduces the tax concession for individuals whose combined income and contributions are greater than the Division 293 threshold.” (ATO, 2023)

Division 293 is triggered if your 293 income and reportable super contributions exceed the current $250,000 threshold.

In this case, it appears that regardless of whether you change the contribution, based on the information provided it appears you will still trigger Division 293.

Given this, you just need to have your situation analysed by an appropriate professional to determine the best type of contribution for your particular circumstances. Your accountant or an accredited financial planner can assist you with this.

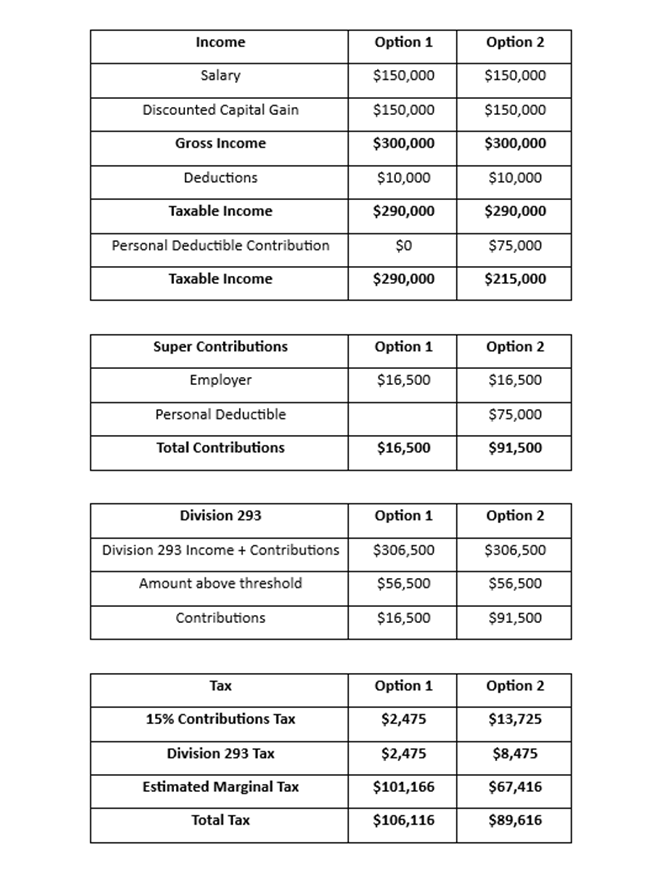

Tax Implications – Case Study

The following case study shows you how to look at the implications of Division 293. In this case the client has $75,000 unused Concessional contributions from previous years and a super balance of $200,00

The net estimated tax benefit is $38,700, with an additional $75,000 (before tax) contributed to their superannuation.

Paul, whilst I was not able to give you specific advice, I hope this information helped. I recommend you seek financial and tax advice in all instances to help you plan for these events and make the best decisions based on you own circumstances.

Best of luck for the future.

While the Adviser Ratings Website facilitates the question and answer functionality, all such communications are between users and authorised financial advisers, of which Adviser Ratings has no affiliation. Adviser Ratings is not the advice provider and does not provide financial product advice and only provides information that is general in nature.

Article by:

Comments0