"I currently pay low amounts on my HELP debt through my compulsory repayments and with upcoming and ongoing CPI increases, the outstanding balance has barely been reduced. Should I make voluntary contributions?"

- Question from Callum in Melbourne, VIC

Top answer provided by:

Paul Wratten

Hi Callum and thanks for your question.

To answer your question, accelerating debt repayment rarely has a downside. Paying off your HELP debt will eventually improve your personal cash flow and your balance sheet, which is useful when trying to achieve other financial goals like home ownership. And the appeal of making voluntary payments to HELP debt is increased as historically high inflation pushes up the balance of these loans.

HELP Debt:

As a quick refresher, HELP stands to Higher Education Loan Program (also known as ‘HECS’ to those who accrued debt prior to 2005) is a loan provided by the Australian government to help cover the cost of higher education. It is an interest-free debt, although outstanding amounts are indexed to inflation.

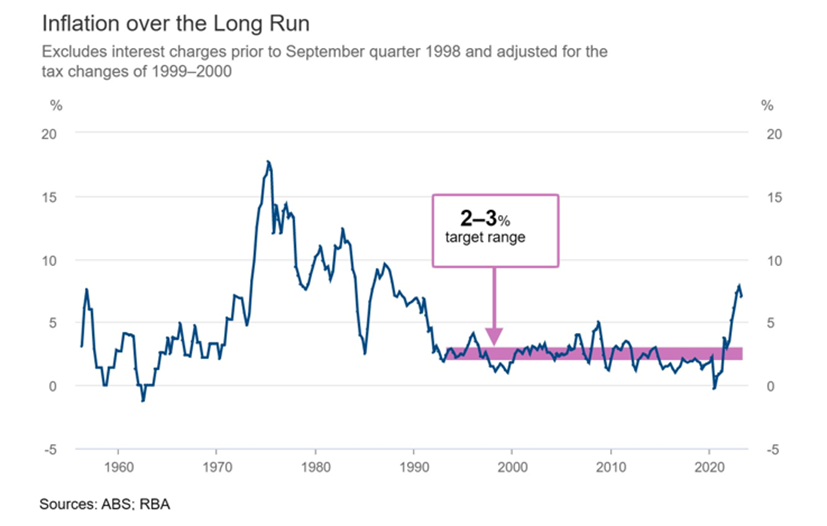

Indexation was fine when inflation bubbled along within the Reserve Banks 2-3% target and we had better things to do with our money. However, this years planned increase of 7.1% (effective 1st June) represents the highest single increase in decades and will raise the average debt by about $1,760 to $26,530.

Figure 1: RBA Inflation over the Long Run

Is your HELP debt shrinking or growing?

I am glad to hear you are making some repayments on your own debt. Compulsory repayments of HELP debt start when personal income reaches the lower threshold of $48,361, with a repayment rate of 1% of your income. The repayment rate increases as your income grows and sometimes this is enough to keep a lid on the debt.

For example, someone with an average HELP debt of $24,770 would need to earn at least $62,739 p.a. (compulsory repayment rate of 3%, so $1,882.17) to effectively cover the 7.1% increase. Their compulsory payments alone would make a small dent in the debt this year, and at least things are headed in the right direction. The size of your HELP debt and your assessable income will determine if your own loan balance reduces or grows year to year.

But paying only compulsory repayments makes eliminating the debt harder in the long term and the ability to make uncapped voluntary contributions has more appeal now than it has done in the past.

Benefits and implications of voluntary contributions:

Increased interest in voluntary contributions seems to centre around reducing or eliminating the impact of the June increase and any future increases. Additionally, paying off debt will improve your cashflow, and your personal balance sheet will look better when you apply for home loans, etc.

But there are some implications to be aware of. For example, your voluntary contributions are locked in so you cannot redraw and reallocate excess payments as you would with a home loan. Future inflation adjustments may not be as sharp as this years, which might reduce the appeal of voluntary contributions. You therefore need to assess alternative strategies that may provide a better outcome before you commit to extra payments.

Alternative 1: Other debt reduction

If you are interested in debt reduction and have other high-interest debt, such as credit card debt or a personal loan, it is a good idea to focus on paying off those debts first before putting extra money towards HELP debt. This is because interest charges on those types of debt are typically much higher than the inflation adjustment on your HELP debt.

Alternative 2: Wealth creation

If you are interested in wealth creation, then Superannuation remains a standout option for improving your overall financial position. Apart from being a great place to grow your money, voluntary contributions to Super can be tax-deductible, and this more strategy may save you more money than the inflation adjustment will cost.

Each of these options have their own benefits and implications. The decision to pay down your HECS debt faster should be based on your individual financial situation and goals, and you will benefit from speaking with a financial advisor to determine the best course of action for your specific situation.

While the Adviser Ratings Website facilitates the question and answer functionality, all such communications are between users and authorised financial advisers, of which Adviser Ratings has no affiliation. Adviser Ratings is not the advice provider and does not provide financial product advice and only provides information that is general in nature.

Article by:

Comments0