“I am 61, planning for retirement next year and will continue to earn some income. I do not need to draw from my super as my partner will continue to work. However, I am looking for guidance on whether to take an income stream from my super or continue with the accumulation phase. The advice I am seeking is about the most beneficial structure for the next 2 years."

-Question from Chris in Leanyer, NT

Top answer provided by:

Orrin Shaw

Hi Chris,

Approaching retirement must be extremely exciting. Selecting the right structure will allow you to focus on enjoying your well-earned retirement knowing that your ‘nest egg’ is positioned to benefit you.

The quick answer in this situation would be to avoid withdrawing funds from your Superannuation if it is not required, as the investment returns being generated will generally be the largest in the years closer to retirement. However, the benefits of a tax-free structure might offset the amount that is required to be released.

The first thing that we need to establish is whether you will be entering full retirement or partial retirement. As you have reached your Preservation Age (over 60) you are eligible to access Superannuation assets, however as you are below the age of 65 you will need to make a ‘retirement declaration’ to be eligible for an Account-Based Pension and the tax-free benefits.

There are two types of Income Streams that are designed to provide vastly different benefits to retirees and pre-retirees:

Account-Based Pension Accounts – An Account Based Pension (ABP) is a retirement income stream that uses Superannuation funds to help retirees meet cashflow requirements during retirement. To be eligible for an ABP account the member must meet a condition of release, either:

- permanent retirement after reaching their Preservation Age; or

- cease an employment arrangement after turning 60; or

- turning 65.

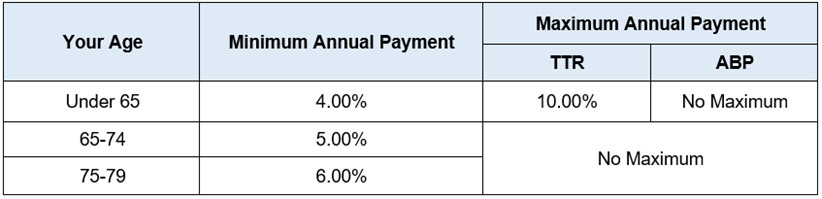

Each year the owner is required to withdraw a minimum amount from the account based on their age at the start of the financial year. There is no maximum withdrawal amount. Once funds enter an account-based pension account they become entirely tax-free (including pension payments, distributions and capital gains generated within the account).

Transition to Retirement Pension Accounts – A Transition to Retirement Pension Account (TTR) is designed to assist members gain access to a portion of their Superannuation funds as they reduce their working hours and offset the reduced income. A TTR account can also assist in providing additional cashflow to make additional tax-deductible contributions. A TTR account has a maximum withdrawal amount of 10% each year based on the account balance at the start of the financial year (E.g. $500,000 balance can access $50,000). Each year the owner is required to withdraw a minimum amount from the account based on their age at the start of the financial year. Pension payments that are made to an owner that is over 60 will be tax-free and won’t form part of the owner’s taxable income. The main difference between a TTR and an ABP account is that a TTR account is still taxed at 15% on all income and earning within the account, similar to an Accumulation Account.

An Accumulation Account is a Superannuation Account that receives contributions (employer or personal contributions) during a member’s working life to accumulate over time and eventually help fund their retirement. Earnings on investments within an accumulation account are taxed at 15% (10% on capital gains).

If you continue to “earn some income” you will not be eligible for an ABP account unless you have ceased your current employment arrangement and started a new employment arrangement. This will act as a condition of release.

In this situation, where income is low, there is basically no benefit to transferring funds into a TTR account as you will not receive any tax benefits and you will be required to withdraw a portion of your retirement funds each year. The tax rates on an Accumulation Account are the same as a TTR account.

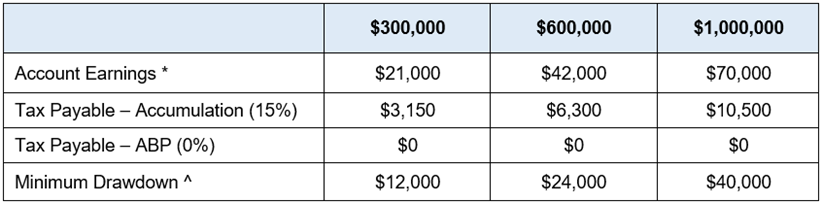

If you are fully retired or have met a condition of release to allow you to transfer your Superannuation funds into an ABP account, the main thing to consider is if the tax that you will save within the tax-free environment outweighs the funds that need to be withdrawn each year (funds can be contributed back into Superannuation until age 75). See below for an estimate of how much tax is saved each year within an ABP account.

*Based on 7% p.a.

^4% minimum drawdown for members under 65.

As there are quite a few moving parts to consider in this situation, I recommend speaking to a Financial Adviser who can provide an accurate recommendation after reviewing your complete financial situation. I hope this information has been helpful and makes your decision easier as you approach retirement.

While the Adviser Ratings Website facilitates the question and answer functionality, all such communications are between users and authorised financial advisers, of which Adviser Ratings has no affiliation. Adviser Ratings is not the advice provider and does not provide financial product advice and only provides information that is general in nature.

Article by:

Comments0