The annual Advice Landscape study, currently underway and having garnered input from nearly 1,000 advisers, reveals a significant shift in advisers' satisfaction with their life insurers. This change follows the implementation of LIF and widespread repricing in the industry, particularly impacting Income Protection products. Advisers are increasingly acknowledging the life insurers' foundational reset efforts and their invitation to engage in writing new business.

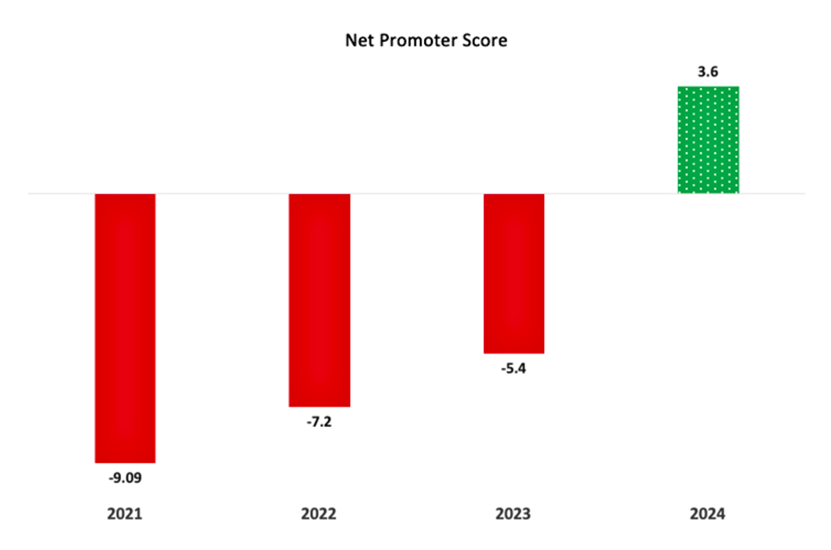

To date, approximately 2,000 insurer reviews from these advisers have resulted in the industry achieving a positive Net Promoter Score (NPS) for the first time since the full implementation of LIF.

Source: Adviser Ratings

Over the past year, there's been a marked increase in the urgency displayed by both regulators and insurers in addressing the chronic underinsurance issue and the consistently low levels of new business. Initiatives such as the formation of the Council of Australian Life Insurers (CALI), the investment in new technologies like LifeBid to enhance operational efficiencies, and APRA's December initiative to open a data transformation consultation project highlight this urgency. These efforts aim to gather more detailed data to help regulators, policymakers, and insurers better understand and manage industry risks. This comes in the wake of APRA's reminder to insurers about their commitments regarding premium increases and the transparency thereof, addressing a key challenge for advisers in persuading clients to renew policies amidst inflationary pressures.

These proactive steps are commendable, yet the challenges remain significant. The real-life implications for advisers are starkly illustrated by the experiences shared by advisers like Kris Chapman. Kris recently recounted on LinkedIn a poignant incident involving a client who was diagnosed with a terminal illness:

“Receiving a call that begins with "I have a brain tumour and only have 6 months to live" is a moment that no financial planner anticipates. In these heartbreaking moments, words often fall short, and all we can do is offer empathy and immediate support.

I recently faced such a call and found myself grateful for a decision made a year earlier. Despite initial resistance, I had convinced the client to retain his life cover. At that point he was still a few years from retirement, financially secure, yet burdened with a significant mortgage and the main breadwinner for the household.”

Similar experiences have been shared by other advisers on social media, including Paul Milbourne and Ross Hultgren.

Having engaged with almost every insurer over the last three months, it's clear that awareness of these challenges is at an all-time high, and concerted efforts are underway. However, questions remain about the patience of many insurers' international parents and the potential role of the government. Is there a need for a fundamental reassessment in this sector?

The critical value and necessity of life insurance become profoundly evident in times of need.

Article by:

Comments1

"I still think that if initial commission rates rise, so that separate advice fees won't need to be charged as much, then the flow of new business should follow."

Bill Hackett 15:53 on 24 Jan 24