The ongoing battle between Retail and Industry funds is about to get hotter, with the industry awakening to the value of financial advice. The space is evolving rapidly driven by continuous government and regulatory impost, commercial pressures, and the changing needs and demands of members. Super funds are set to take an increasingly influential role in providing financial advice to captive members - so what does this mean for advisers and their clients?

The ongoing battle between Retail and Industry funds is about to get hotter, with the industry awakening to the value of financial advice. The space is evolving rapidly driven by continuous government and regulatory impost, commercial pressures, and the changing needs and demands of members. Super funds are set to take an increasingly influential role in providing financial advice to captive members - so what does this mean for advisers and their clients?

For various reasons, the majority of advisers have traditionally favoured Retail funds when advising their clients. This preference seems set to be confronted by industry super players who have woken to the value that advice can bring to their members, who are increasingly looking for full suite advice in their efforts to secure their long term financial security. There are trillions of dollars at stake.

Retail vs Industry

In the market battle between Retail and Industry funds, Retail funds have been preferred super vehicle for financial advisers, particularly those owned or aligned under the Big Six that provide their own branded super funds. Retail funds have invested significantly in building brand awareness within the financial advice community, and most importantly in terms of successful distribution through the advice channel, ensuring their products are featured on administration platforms and advice licensee APLs. Advisers within privately owned licensees are more likely to advise on public sector and industry funds than their non-privately owned counterparts.

Fig 1: Proportion of Advisers Able To Advise On Super Fund Types (Adviser Ratings 2018 Landscape Report)

Industry funds, established for employees of a particular industry and typically enshrined through industrial awards, have benefitted from “default” arrangements, although these are being challenged by the Coalition Government and considered as part of a review by the Productivity Commission into super industry efficiency.

However, a number of Industry funds are now open for anyone to join, which reflects a bigger game that involves a race for scale, driven by commercial realities and entreaties from regulators, witnessed by a number of fund acquisitions and mergers over the last decade.

Opportunity for Advisers

The larger industry funds are waking up to the importance of financial advice for members and building more complex advice business plans that include substantially greater engagement with the external advice community.

With choice and technology making switching and consolidation easier than ever, super funds can no longer take members for granted. As such, super funds are progressively tackling the perpetual challenge of raising member awareness and engagement with superannuation to improve retention. As figure 1 shows, nearly $1.2 trillion in investor funds are currently wrapped up in Public Sector and Industry Funds.

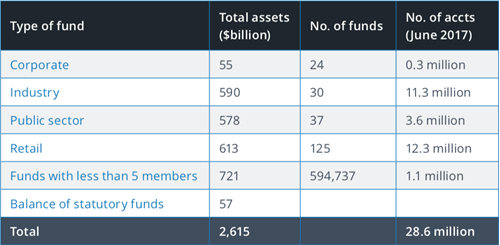

Fig 2. Super Fund Industry Summary (Source APRA Dec Qtr. Statistics)

Retention of members approaching retirement is increasingly important to super funds, both in order to maintain their revenue base by transitioning accumulation members into retirement products offered by the fund and, more benevolently, to ensure life-time stewardship and care for members.

With regard to member retention strategies, it is generally accepted that provision of financial advice is one of the best methods, while at the same time ensuring members achieve greater financial security longer-term. With 23% of Australians in the 55 to 64-year age bracket seeking advice while also holding the highest average super fund balance, the battle for the nearly-retired investor is heating up.

Industry Funds and Advisers

Industry funds are building more sophisticated financial advice strategies, and have increased their employed adviser numbers by 54% to 565 advisers in recent times. However, this roughly equates to one financial adviser per 15,000 industry fund members, which is patently too low to service even a fraction of the member base.

They are however recognising they need better adviser coverage and to expand their advice offering from intra-fund advice to comprehensive advice delivered in scale. They are pursuing this by increasing the number of employed advisers and, particularly for the larger funds, building panels of accredited advisers from “industry fund-friendly” licensees.

In offering more comprehensive advice, industry super funds will themselves need to build out their own non-super investment APLs and financial product manufacturers will need to be alert to these developments. Those fund managers that are already managing investment mandates for the super fund, provided they offer retail managed funds, would seem to have a natural advantage.

Furthermore, in outsourcing much of the comprehensive advice, industry super funds are establishing increasingly rigorous screening processes to ensure they find the best advisers and advice firms for their members. And for good reason - while not authorised under the super fund AFSL, these advisers nevertheless represent potential reputational risk for the super fund. These screens may include review of organisational values, business strength, compliance records, and adviser quality. In the future, we anticipate super funds may also take an increasing interest in the APL make-up of these firms.

If this direction from industry funds is sustained, and if the banks persist with their intentions to exit the wealth management sector, the architecture of the superannuation advice landscape will be fundamentally transformed, though the problems regarding conflict of interest and vertical integration may remain – albeit with different players. Would consumers benefit any more from advisers being “aligned” to a small number of industry superfunds than they do by advisers being aligned with banks?

Regardless, these developments should be a wakeup call for the Retail funds who traditionally had favour with 90%+ of financial advisers, particularly those aligned under the same parent company owning the super fund. As industry funds extend their push into the privately owned advice channel, retail funds will face new challenges to their dominance with advisers, in addition to their long-running competition for the hearts and mind of consumers particularly through the “Compare The Pair” advertising campaign.

by Angus Woods, MD, Adviser Ratings

Article by:

Comments7

"I actually received a call from a marketing agency recently who were performing research on behalf of QSuper, who were investigating the likelihood an adviser would use them more if they had facilities to better allow advisers to work with members of the fund. It was nice to hear that another fund is opening up for advisers to help their clients!"

Grant 07:42 on 07 Jun 18

"Yes, I work for a bank and yes I have an APL just like any other business does with preferred suppliers because that's due diligence. When a client comes to me with existing superfund that is outside my APL and it is in the best interest of the client to retain that fund, then that is what I recommend. The frustration is in trying to service that client when the fund only allows preferred advisers access to its members accounts and you have to jump hoops even with an authority to get client information. All funds need to open up to all advisers to make it easier for their members to stay with them and keep their preferred adviser."

LV 18:00 on 06 Jun 18

"The compare the pair ads will also be incorrect, as they assume that there is no advice cost being deducted from the industry fund member, which there now will be. Under FASEA, good luck finding an adviser, as you wont be able to afford them. "

SB 16:10 on 06 Jun 18

"If government was looking at the best interests of all clients, then they should make it mandatory that an adviser can charge there fees to any super fund. At present not all industry funds allow this"

KB 15:47 on 06 Jun 18

"if this happens superfunds will just be the new banks re vertical intergration and conflicts of interest"

Tegan Mansfiel 15:42 on 06 Jun 18

"If advisers are no longer preferencing bank retail funds, they will have to start performing a whole lot better or face new funds drying up. Their fees will have to drop or their returns will have to be better if they're to justify their existence on a level playing field."

Loaded 15:39 on 06 Jun 18

"When Banks exit advice there will be a new mini (maxi?) industry that pops up to push all sorts of product to advisers who were previously recommending bank gear. The fragmentation of the industry will mean its much harder to police than it was."

DM 15:30 on 06 Jun 18